Table of Content

Before joining CNET Money, Wojno was Senior Editor of Finance for ZDNet, writing on blockchain, cryptocurrency, financial services, investing and taxes. Outside the digital world, Marc can be found spinning vinyl, threading reel-to-reel tapes, shooting film with his Bolex and hosting an occasional pub quiz. Alix is a staff writer for CNET Money where she focuses on real estate, housing and the mortgage industry. She previously reported on retirement and investing for Money.com and was a staff writer at Time magazine. She has written for various publications, such as Fortune, InStyle and Travel + Leisure, and she also worked in social media and digital production at NBC Nightly News with Lester Holt and NY1.

And if the Federal Reserve decides to slow down on rate hikes, as Fed Chair Powell hinted on December 1, we could see further declines (or at least a leveling-off) in the future. Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next. And here are some reasons why a 20-year mortgage may not make as much sense as a 30-year home loan. Mortgage rates may increase by the end of the year, so if you're looking for a new home it could make sense to buy now, rather than waiting.

Year Refinance Rates

Use our mortgage refinance calculator to get a better idea if now if the right time to refinance for you. If you took out a $300,000 home loan with a 30-year fixed rate of 5.5%, you’d pay around $313,000 in total interest over the life of the loan. The same loan size with a 15-year fixed rate of just 5.0% would cost only $127,000 in interest — saving you around $186,000 in total. A credit score of 620 or higher might qualify you for a conventional loan, and — depending on your down payment and other factors — potentially a lower rate.

The 15-year forces greater discipline & allows outright ownership of the home in half the time. Comparing 20-year mortgage rates across different lenders, you can see what rates, terms, and loan amounts you qualify for. In turn, you can snag the 20-year mortgage rates with the lowest interest rates, flexible repayment terms by comparing quotes from lenders. Nevertheless, you should not solely rely on the interest rate when determining whether it is time to refinance. You’ll also need to weigh how long you have left to pay off your current mortgage and to consider the repayment term of a new home loan.

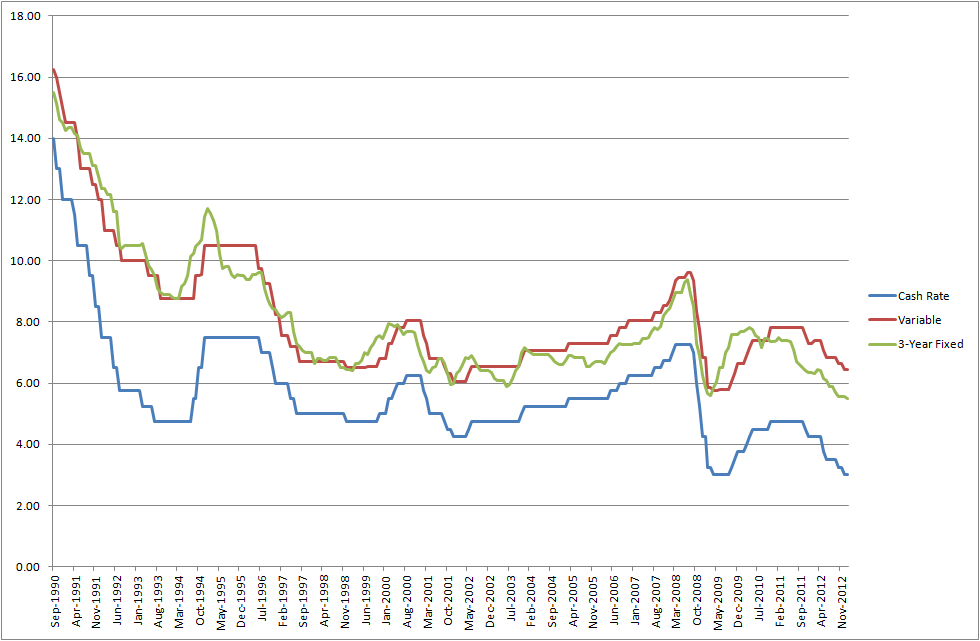

Historic mortgage rates: Important years for rates

For example, a borrower with a $120,000 mortgage could reduce the principal and interest payment on their mortgage from $1,809 to $966 per month by refinancing from an 18% rate to a 9% rate. The low-rate environment created a refinancing boom, with rates briefly dropping below 7% for most of 1998 — allowing many owners to refinance multiple times. When refinancing a mortgage, a 20-year term is a great choice because choosing it means you don’t need to start all over again with a 30-year mortgage. While a 30-year term could mean a lower monthly payment, you’ll end up paying more in interest overall, defeating the purpose of refinancing in the first place.

While we adhere to strict editorial integrity, this post may contain references to products from our partners. Stability – You’ll be able to lock in the interest rate on your mortgage for the entire 20-year term. This gives you a degree of predictability you won’t have with an adjustable-rate mortgage . So we give you the opportunity to compare deals offered by the banks and choose the one with the most favourable interest rates.

Pros of a 20-year fixed-rate mortgage

Since it's a shorter loan term you will end up paying a full decade less in interest, which adds up to tens of thousands of dollars in savings. Bankrate has been the authority in personal finance since it was founded in 1976 as the “Bank Rate Monitor,” a print publication for the banking industry. Bankrate has been surveying and collecting mortgage rate information from the nation’s largest lenders for more than 30 years. A 20-year fixed-rate mortgage is a home loan that has a repayment period of 20 years.

Of course, all of this depends on how many years you have left on your current mortgage and the amount you want to refinance. That’s why it’s best to shop around to see what makes the most sense for your financial situation. A 20-year mortgage works the same way as 15- and 30-year mortgages, it just has a 20-year term instead.

Down payment

Keep in mind that mortgage rates may change daily and this data is intended to be for informational purposes only. A person’s personal credit and income profile will be the deciding factors in what loan rates and terms they are able to get. Loan rates do not include amounts for taxes or insurance premiums and individual lender terms will apply. In order to assess the best 20-year mortgage rates, we first needed to create a credit profile. This profile included a credit score ranging from 700 to 760 with a property loan-to-value ratio of 80%.

To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. Before you apply, try to get your credit score in the best shape possible and make sure you have all your paperwork ready. Mortgages lasting 20 years aren’t as common as 30-year mortgages, but they can be a very smart choice.

When moneys are fluid, for example during an economic upturn where financial institutions have abundant resources, some loans may be advertised as free to the borrower. These loans may seem attractive to the borrower but often come at a higher interest rate than other mortgage plans. One way or another you still end up covering the bank's costs & profit margin. Typically a new loan will include a series of fees including points which are 1% of the loan amount and paid at the time of funding to secure a lower interest rate. Some lenders allow points to be amortized over the life of the loan. Thirty-year fixed-rate mortgages are popular with homebuyers because they provide the stability of a fixed, low monthly payment.

For the remainder of the decade, rates stayed in the 3.45% to 4.87% range. The average 30-year fixed-refinance rate is 6.54 percent, down 13 basis points compared with a week ago. A month ago, the average rate on a 30-year fixed refinance was higher, at 6.88 percent. Lower monthly payments can free up some of your monthly budget for other goals, like building an emergency fund, contributing to retirement or college tuition, or saving for home repairs and maintenance. The average 30-year fixed-mortgage rate is 6.47 percent, a decrease of 16 basis points over the last week.

Compared to a 15-year or 10-year refinance, a 20-year term is much more doable in terms of the monthly payment amount. Lenders offer mortgage points to give borrowers the option to prepay interest when taking out a home loan. This one-time fee is also referred to as discount points and is intended to lower a borrower’s interest rate. To lower the rate by a quarter of a percent, it’ll cost you one percent of your mortgage amount. For example, if you take out a $250,000 mortgage and you want to lower the current interest rate of 3.25% by one point, you’ll need to pay $2,500 to get it down to 3%.

A fixed 20-year mortgage is a loan lasting for 20 years, or 240 monthly payments, with an interest rate that stays consistent for the duration of the loan. For example, on a 20-year mortgage for a home valued at $300,000 with a 20% down payment and an interest rate of 3.75%, the monthly payments would be about $1,423 . Because the loan amount and interest rate stay the same, principal and interest payments remain flat for the 20-year term. A 20-year fixed rate mortgage is a home loan with an interest rate that remains the same throughout the 20-year duration of the loan. The borrower will be required to repay the principal and interest on the loan throughout the course of 20 years. Note that while the payments will be the same amount for 20 years, in the initial years, a higher part of the payment goes towards interest payments rather than towards the principal.

No comments:

Post a Comment